A mortgage rate buydown is when money is used upfront to reduce a buyer’s interest rate, either temporarily or permanently. That money can come from the seller, the builder, the buyer, or in some cases from a buyer commission rebate. A rate buydown can reduce your monthly payment, lower your cash-to-close burden in the early years, or improve affordability enough to help make a purchase work.

For many buyers, especially in a higher-rate environment, understanding how a mortgage rate buydown works can save thousands of dollars and help answer one of the most important questions in real estate: is it better to reduce the purchase price, get seller concessions, or use credits to buy down the rate? You can also estimate how much you could save depending on price point and available credits.

At EZ Agents, we help buyers think through these tradeoffs in real numbers. In many cases, our 50% commission rebate can be used at closing in a way that helps reduce your out-of-pocket costs. You can also learn more about how our Denver rebate realtor model works and why so many buyers choose a more modern approach to home buying.

What is a rate buydown?

A rate buydown is a financing strategy where money is paid upfront to reduce the mortgage interest rate. The reduced rate lowers the buyer’s monthly principal and interest payment. Depending on the structure, the lower rate may last for the full life of the loan or just for the first one to three years.

There are two main types of mortgage rate buydowns: temporary buydowns and permanent buydowns. Both can be useful, but they work differently and are best suited to different kinds of buyers.

Temporary vs. permanent rate buydowns

Temporary rate buydown

A temporary buydown lowers the interest rate for an initial period, typically the first one, two, or three years of the loan. A common example is a 2-1 buydown, along with other structures like a 3-2-1 buydown.

For example, with a 2-1 buydown, the buyer’s rate is reduced by 2% in year one and 1% in year two before returning to the full note rate in year three. This can make the first couple of years of ownership much more affordable.

Permanent rate buydown

A permanent buydown reduces the interest rate for the entire life of the loan. This is usually done by paying discount points upfront. One point generally equals 1% of the loan amount, though the exact cost and rate reduction vary by lender and market conditions.

A permanent buydown may make sense for buyers who expect to keep the home and mortgage for a long time. A temporary buydown may make more sense for buyers who want lower payments now or believe they may refinance later.

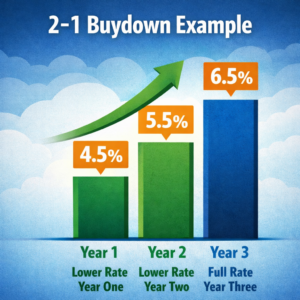

Example of a 2-1 mortgage rate buydown where the interest rate is reduced in year one and year two before returning to the full rate in year three.

How does a 2-1 buydown work?

A 2-1 buydown is one of the most common temporary buydown structures. The mortgage is still underwritten at the full note rate, but the buyer gets a reduced payment in the first two years.

Example:

Note rate: 6.5%

Year 1 payment based on: 4.5%

Year 2 payment based on: 5.5%

Year 3 and beyond payment based on: 6.5%

The funds needed to cover the payment difference are typically paid upfront by the seller, builder, or another allowable source at closing. This is why seller concessions can be so valuable in a buyer’s market. They may not lower the sticker price of the home, but they can make the payment meaningfully lower when it matters most.

Who pays for a rate buydown?

A mortgage rate buydown can be funded in several ways:

- Seller concessions negotiated in the contract

- Builder incentives on new construction homes

- Buyer funds brought to closing

- In some cases, a buyer commission rebate that is properly disclosed and approved by the lender

This is one reason many buyers ask about commission rebates in Colorado. If you are already working with a rebate realtor, that money may help offset closing costs, prepaid items, or other approved expenses at closing depending on the loan and lender guidelines.

Rate buydown vs. price reduction

A common question from buyers is whether it is better to negotiate a lower purchase price or use seller concessions to buy down the rate. The answer depends on the size of the credit, the buyer’s loan type, how long they expect to keep the mortgage, and their monthly payment goals.

In many cases, a rate buydown can create more immediate monthly relief than a modest price reduction. A small drop in purchase price may not dramatically change the monthly payment, but the same amount applied toward a temporary or permanent buydown can sometimes have a more noticeable short-term effect.

That is why buyers should evaluate all three together: purchase price, seller concessions, and any available rebate. A smart strategy is often less about chasing the lowest headline price and more about structuring the deal in a way that best improves affordability.

A $20,000 credit can be used as a price reduction or a rate buydown, but applying it toward a buydown can often create greater monthly payment savings.

In many cases, applying credits toward a rate buydown can reduce your monthly payment more than a similar price reduction.

Rate Buydown vs. Price Reduction Example on a $750,000 Home

| Scenario | Credit Used | Primary Impact | Monthly Payment Effect | Best Fit |

|---|---|---|---|---|

| Price Reduction | $20,000 | Lowers purchase price and loan balance slightly | Usually modest monthly savings | Buyers focused on long-term principal reduction |

| Rate Buydown | $20,000 | Reduces interest rate instead of purchase price | Often stronger monthly payment relief | Buyers focused on affordability and cash flow |

| Seller Concession Buydown | $20,000 seller credit | Keeps price the same but applies negotiated credit at closing | Can meaningfully reduce payment | Buyers with leverage in negotiation |

| Commission Rebate Buydown | Buyer agent rebate applied at closing | Uses available rebate to offset approved closing costs or financing strategy | Can improve affordability depending on lender approval | Buyers using a rebate realtor model |

| Combined Strategy | $20,000 seller credit + commission rebate | Stacks multiple savings sources to maximize flexibility | Can create the biggest payment and cash-to-close benefit | Buyers focused on maximizing total savings |

In many cases, applying the same credit toward a rate buydown can reduce monthly payments more than a price reduction, especially in higher price ranges.

The main takeaway is that the same dollar amount can have a very different effect depending on how it is used. In many cases, applying credits toward a rate buydown can reduce a buyer’s monthly payment more than using that same amount as a price reduction. And when seller concessions and a commission rebate can be combined, the savings can be even more meaningful.

Key Takeaway:

A $20,000 credit used for a rate buydown often creates more immediate payment relief than the same $20,000 price reduction. Buyers should compare both options along with seller concessions and commission rebates.

Can you use seller concessions for a rate buydown?

Yes, in many cases seller concessions can be used to fund a mortgage rate buydown. This is especially common when homes have been sitting longer, when builders are offering incentives, or when buyers have leverage in negotiations. The lender will still need to approve how credits are applied, and concession limits can vary by loan type.

If you are buying a resale home, seller concessions may be one of the best negotiating tools available. If you are buying new construction, builder incentives may create similar opportunities. We often talk through these scenarios with buyers who are also comparing discount realtor options in Denver and trying to decide how to save the most money on the transaction overall.

Can you use a commission rebate for a rate buydown?

Potentially, yes. A commission rebate is typically handled as a credit at closing and must be properly disclosed on the settlement statement. Whether it can be used directly toward a rate buydown depends on the lender, loan program, and how the closing credit is being applied.

For financed buyers, lender approval matters. For cash buyers, things are often simpler. Either way, this is one of the reasons buyers working with EZ Agents often want to understand the full picture before writing an offer. A rebate is not just a nice bonus. It can be part of a larger strategy to reduce cash to close, offset transaction costs, and improve overall affordability.

If you are early in your search, you may also want to review our home buyer savings calculator to get a rough idea of how much a rebate could be worth based on price point and commission structure.

When does a rate buydown make sense?

A mortgage rate buydown may make sense when:

- The buyer wants a lower monthly payment right away

- The seller or builder is offering meaningful concessions

- The buyer expects rates may improve and refinance could be possible later

- The buyer plans to hold the mortgage long enough for a permanent buydown to pay off

- The buyer wants to use available credits strategically rather than only focusing on price

A buydown is not always the best answer. Sometimes lowering the purchase price, preserving cash reserves, or using credits for other closing expenses will be the smarter move. But for many buyers, especially in higher-rate conditions, a well-structured buydown can be one of the most helpful tools available.

Rate buydown strategy for Colorado home buyers

Colorado buyers should think about rate buydowns as part of the overall negotiation, not as a separate lender-only topic. The financing side matters, but so does how the offer is written, what concessions are requested, and whether there are other savings opportunities available in the transaction.

That is where an experienced agent can add real value. A smart buyer strategy is not just about finding the home. It is about structuring the deal properly. That includes price, inspection, seller credits, builder incentives, and how your agent’s compensation model may affect your bottom line.

At EZ Agents, buyers find the home online, we handle the contracts, negotiations, inspections, and closing process, and then we split our commission 50/50. If you want to better understand how that works, visit our about page, read our reviews, or contact us to talk through your specific situation.

Frequently Asked Questions About Mortgage Rate Buydowns

What is a mortgage rate buydown in simple terms?

A mortgage rate buydown is when money is paid upfront to reduce the buyer’s interest rate, which lowers the monthly mortgage payment.

What is the difference between a temporary and permanent rate buydown?

A temporary buydown lowers the rate for the first one to three years. A permanent buydown lowers the rate for the full life of the loan.

What is a 2-1 buydown?

A 2-1 buydown lowers the interest rate by 2% in year one and 1% in year two before returning to the full note rate in year three.

Who usually pays for a rate buydown?

The seller, builder, buyer, or another approved source can fund a rate buydown, depending on the loan and transaction structure.

Can seller concessions be used for a rate buydown?

Yes, in many cases seller concessions can be used to fund a temporary or permanent mortgage rate buydown, subject to lender and loan guidelines.

Can a commission rebate be used for a rate buydown?

Sometimes. A commission rebate may be able to help offset closing-related costs, but how it can be applied depends on the lender, loan type, and approval requirements.

Is a rate buydown better than a price reduction?

Not always. A rate buydown can provide stronger monthly payment relief, while a price reduction lowers the loan balance. The better option depends on the numbers and the buyer’s goals.

When does a permanent rate buydown make sense?

A permanent buydown often makes more sense when the buyer expects to keep the home and mortgage for a long time and wants stable payment savings over the life of the loan.

When does a temporary buydown make sense?

A temporary buydown may make sense when a buyer wants lower payments in the first few years, expects income to rise, or thinks refinancing may be possible later.

Can a rate buydown help make a home more affordable?

Yes. Lowering the interest rate can reduce the monthly payment, which may improve affordability and make ownership more manageable in the early years.